Proactive risk management can protect fuel buyers facing geopolitical influences on petroleum prices.

2026 has already proven to be a turbulent year for oil markets. The year began with the US invasion of Venezuela in January, which initially raised expectations that additional barrels of crude oil could be returning to the global market. However, attention quickly shifted to a far more disruptive development: the US-Israel military strikes on Iran and Iran’s retaliation, which have threatened energy flows through the Strait of Hormuz and have triggered a sharp rally across petroleum futures.

US-Israel-Iran Conflict Pushes Oil Higher

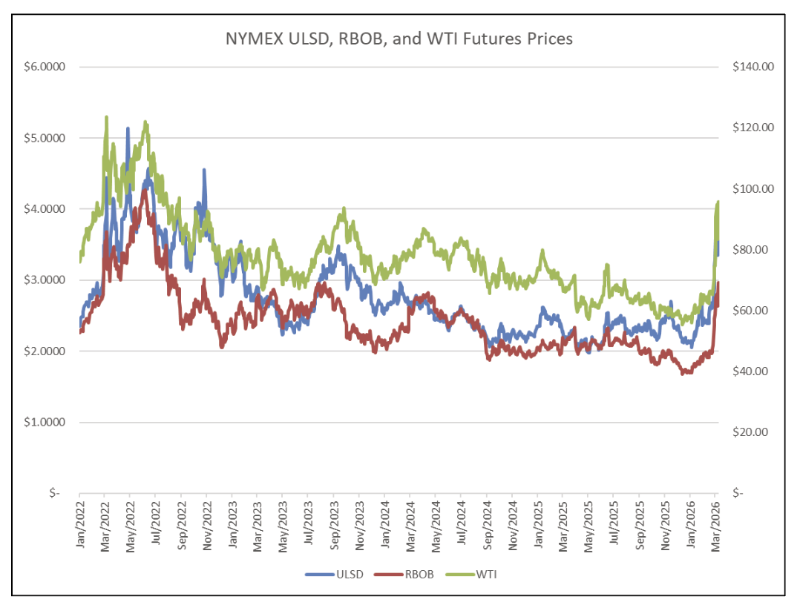

Crude oil, gasoline, and distillate futures have all surged in early March (at the time of this writing), with both WTI and Brent crude oil prices briefly pushing above $100 per barrel (bbl) as tensions escalated in the Middle East. The rally has been driven primarily by fears surrounding the Strait of Hormuz. The narrow waterway connecting the Persian Gulf to the Gulf of Oman is one of the most important transit routes in global energy trade. Roughly 20 million barrels per day (mb/d), or about 20% of global supply of crude oil and refined products, pass through the strait.

In late February and early March, military strikes in the region involving US and Israeli forces targeting Iranian assets – followed by Iranian strikes on neighboring countries - impacted commercial shipping activity, resulting in slower tanker movements amid rising insurance costs, security risks, and operational uncertainty.

Oil markets that had traded within relatively stable ranges for much of 2025 suddenly experienced some of their largest daily moves since 2022, when the conflict between Russia and Ukraine began.

From Supply Growth to Supply Risk

The International Energy Agency (IEA) had spent much of 2025 forecasting one of the largest potential supply surpluses in oil market history for 2026 – exceeding 4mb/d. With traders also focused on the possibility that Venezuelan oil production could eventually increase following the easing of certain sanctions, this remained the prevailing market view at the beginning of the year.

However, that narrative was quickly overshadowed by events in the Middle East. The shift from supply growth to supply risk has been the key reason petroleum futures rallied in recent weeks.

Reports began to emerge that several producers in the region - such as Iraq, Kuwait, and the United Arab Emirates - were curtailing output as export logistics became increasingly difficult. With tanker traffic through the Strait of Hormuz slowing significantly, storage at export terminals began filling up rapidly, forcing some fields to reduce production until shipments could resume.

In addition, Saudi Arabia, the world’s largest crude oil exporter, began preparing to redirect some exports away from the Persian Gulf towards the Red Sea using its East-West pipeline system. However, the pipeline cannot fully replace the volumes typically shipped through the Gulf. At the same time, the US signaled that it would allow India to continue importing Russian crude oil despite sanctions for a limited time, in an effort to maintain supply flows to global markets.

Strategic Reserve Release

On March 11, members of the IEA agreed to release 400mb of crude oil from strategic reserves, representing the largest emergency release in the organization’s history. The US alone agreed to release 172mb from its Strategic Petroleum Reserve, which at the time of this writing held roughly 415mb. While these releases cannot fully replace lost production in the event of a prolonged disruption through the Strait of Hormuz, they can help bridge short-term supply gaps and reduce price spikes.

Market Outlook: Volatility Likely to Persist

The trajectory of petroleum futures will depend heavily on the duration and severity of the Middle East conflict. If shipping through the Strait of Hormuz remains constrained, the market could see further pressure on prices. Some analysts have warned that crude oil prices could reach $150/bbl, particularly if inventories begin to decline rapidly.

However, governments have already agreed on large oil releases from strategic petroleum reserves, which are expected to inject hundreds of millions of barrels into the market. Moreover, higher prices tend to lower demand and encourage production outside the Gulf region. As a result, it is likely that the market will remain highly volatile in the coming months amid the uncertainty.

Managing Risk

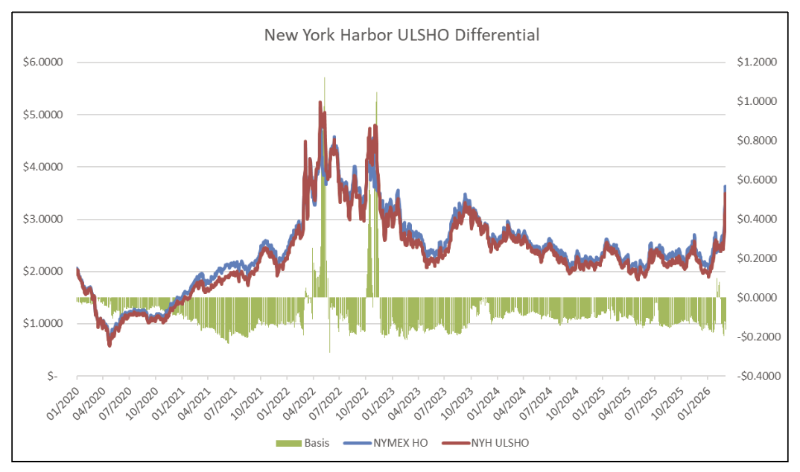

When futures prices become unstable, managing basis exposure becomes critical. Many fuel buyers hedge the futures component of their price exposure using NYMEX contracts, but the physical price they ultimately pay depends on a differential to the local market. That differential – often referred to as basis – can move independently of futures and introduce additional price risk. One strategy to mitigate this risk is to lock in fixed differentials with a supplier.

Under this strategy, the buyer agrees to a predetermined differential to a benchmark futures contract. This structure removes much of the uncertainty surrounding local supply conditions and ensures the buyer understands how the physical price will move relative to futures. One important detail, however, which is often overlooked, is that the differential should correspond to the month in which the product is lifted, rather than the preceding month. Using the incorrect month can create unintended exposure to calendar spreads between futures contracts. By ensuring that the differential matches the delivery month, buyers can avoid this complication and keep the hedging structure straightforward.

If the first few months of 2026 have illustrated anything, it is how quickly market narratives can shift. What began as expectations that Venezuelan supply might gradually return to the global oil markets quickly shifted to concerns over geopolitical tensions in the Middle East and potential supply disruptions in the Strait of Hormuz. For fuel buyers, this shift highlights the strong influence of geopolitical risk on petroleum prices and the importance of proactive risk management.

Consultants at Hedge Solutions bring decades of experience helping clients navigate these market dynamics through disciplined hedging, purchasing, and marketing strategies. With a structured approach to risk management and proprietary analytical tools, we help clients make informed procurement decisions even during periods of significant market volatility.

Anja Ristanovic is a Financial Analyst at risk management consultancy Hedge Solutions. She can be reached at 800-709-2949.

The information provided in this market update is general market commentary provided solely for educational and informational purposes. The information was obtained from sources believed to be reliable, but we do not guarantee its accuracy. No statement within the update should be construed as a recommendation, solicitation or offer to buy or sell any futures or options on futures or to otherwise provide investment advice. Any use of the information provided in this update is at your own risk.