Key takeaway: As little as 20 percent of the ‘Section 45Z’ tax credit value flows through the supply chain to blenders and consumers, whereas with the Biodiesel Tax Credit, between 50 percent and 70 percent of the credit value passed to blenders and consumers.

Via Press Release: NATSO

A new independent study finds that the Section ‘40A’ Biodiesel Blenders’ Tax Credit (BTC) delivers significantly more value across the entire biofuel supply chain than its replacement, the ‘Section 45Z’ Clean Fuel Production Credit.

The report, commissioned by NATSO, representing America’s travel centers and truck stops, SIGMA: America’s Leading Fuel Marketers, and the National Association of Convenience Stores (NACS); and prepared by GlobalData, a leading energy research and analytics firm, finds that nearly 70 percent of the Biodiesel Tax Credit value flowed through the supply chain to blenders and consumers, ranking it among the most consumer-friendly biofuel policies.

The report, titled, “Tax Credit Impact on U.S. Biofuels,” analyzes the impact of biofuel tax credits and how their value is shared throughout the supply chain to the benefit of farmers and consumers.

“This study highlights that the Biodiesel Tax Credit remains one of the most consumer-oriented tax policies, with the vast majority of its value trickling down into lower prices at the pump,” said NATSO President and CEO Max McBrayer. “This reaffirms our industry’s position that reinstating the Biodiesel Tax Credit represents a common-sense solution for ensuring stable fuel supply options while also helping to lower fuel prices at the pump.”

Conducted by GlobalData, the research examined the ‘40A’ Biodiesel Benders’ Tax Credit that expired at the end of 2024, and the existing ‘Section 45Z’ Clean Fuel Production Credit to compare how these tax credits influence demand for biofuels and ultimately impact the market.

“The study’s findings confirm what fuel retailers see every day: reducing fuel costs at the point of blending means greater savings at the pump,” said Matt Durand, Deputy General Counsel for NACS. “The 40A credit is a transparent and market-tested way to help lower diesel prices, delivering real value for American families and small businesses.”

Using independent data, GlobalData found that as little as 20 percent of the ‘Section 45Z’ tax credit value flows through the supply chain to blenders and consumers.

When the Biodiesel Tax Credit was in place, between 50 percent and 70 percent of the credit value passed to blenders and consumers. By comparison, under the existing ‘Section 45Z’ Clean Fuel Production Tax Credit, just 20 percent to 40 percent of the credit value flows to blenders and consumers with producers retaining up to 80 percent of the value.

NATSO, SIGMA and NACS, which represent 90 percent of fuel sold at retail, urge Congress to quickly reinstate the Biodiesel Tax Credit. The Biodiesel Blenders’ Tax Credit represents a significant opportunity to help stabilize diesel prices and strengthen demand for renewable fuels – enhancing supply options and alleviating fuel price pressures caused by today’s market volatility and geopolitical risks.

As surrogates for the consumer, when fuel retailers pay less to buy and blend biofuel, they are incentivized to pass those savings on to customers in the form of lower prices at the pump. The structure of the ‘45Z’ credit makes it impossible for fuel retailers to access savings and extend those benefits to consumers.

The longstanding ‘40A’ Biodiesel Blenders’ Tax Credit was replaced in 2025 by the ‘Section 45Z’ production credit. The simple $1 per gallon blender credit was eligible for all biomass-based diesel. The ‘Section 45Z’ credit, by comparison, is a complex income tax credit that varies based on greenhouse gas emissions and must be redeemed by producers against their annual tax filings.

According to the Executive Summary provided:

Under a blender’s tax credit, more value is added to the supply chain, and the mechanism means it is relatively evenly spread throughout the supply chain. The impact on consumption is limited.

- BTC - In “normal” years, producers were able to keep 30-50 percent of the credit value and 50-70 percent of the credit value flows to blenders and consumers.

The producers’ tax credit adds less value to the supply chain. The value will be unevenly spread along the chain, with more value kept by the biodiesel producer, and less passed along the chain. The impact on consumption is limited but this credit boosts demand for domestic production and feedstocks.

- 45Z - In “normal” years, producers should be able to keep 60-80 percent of the credit value. However, the majority of biofuel producers will trade these credits to other businesses, losing 5-10 percent of the value from the biofuel supply chain.

- For U.S. RD produced from qualifying feedstocks, producers have retained 80-100 percent of the tax credit value.

- As an income tax credit, producers only receive the value periodically, after volumes have been produced. This prevents the value being passed down to consumers through lower prices.

- The remaining 20-40 percent of the credit value flows to blenders and consumers.

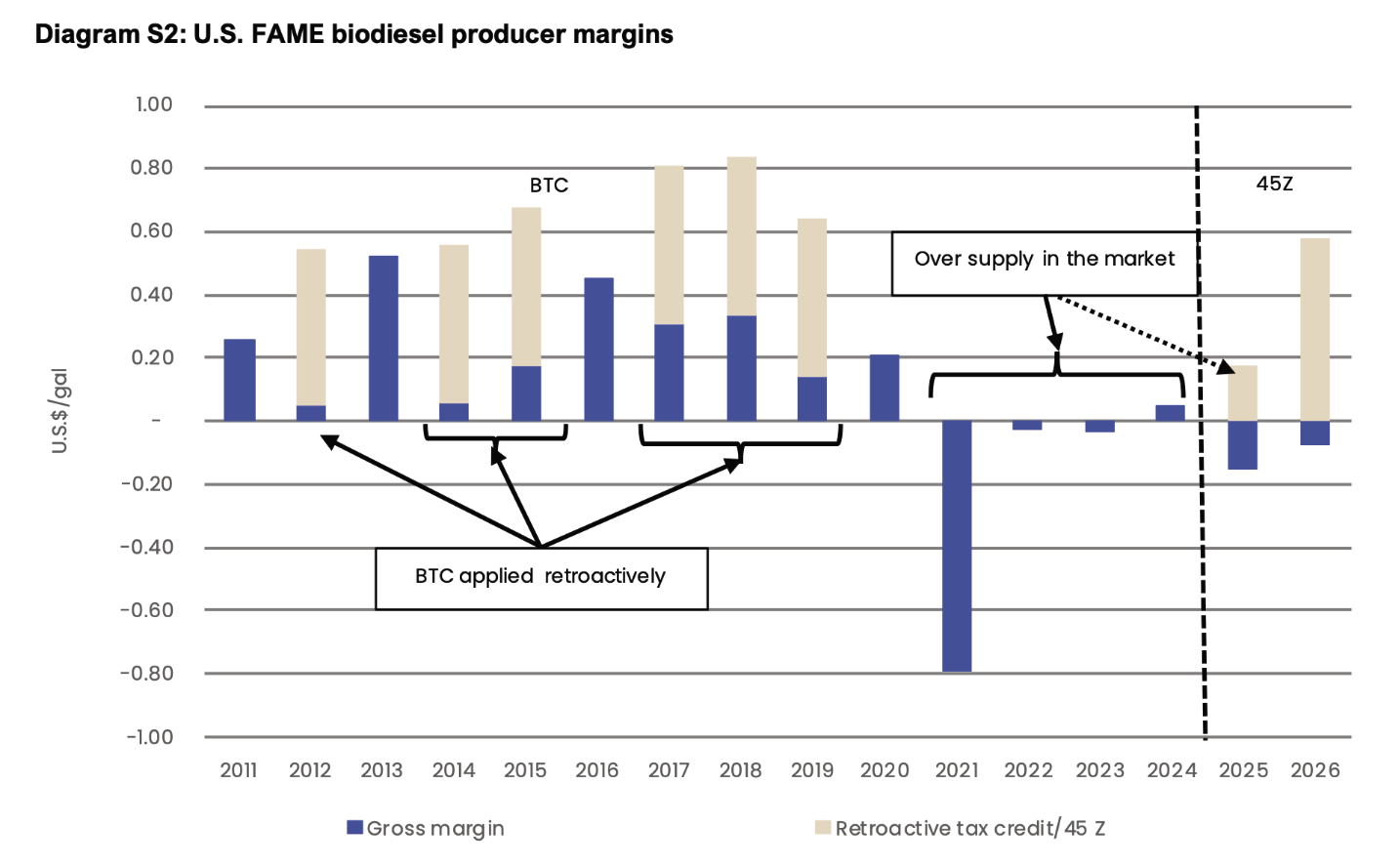

Under both tax credit systems, market fundamentals play a key role in where the credit value flows to in the supply chain. In years where the BTC was applied retroactively a $0.50/gallon payment is shown, however, in later years this likely overstates the payment as blenders took more of the risk as expectations of a reinstatement of the credit became more certain. The 45Z tax credit for soy-based FAME biodiesel is shown for 2025 and 2026 (assumed $0.33/gallon in 2025 and $0.60/gallon in 2026 under new calculations excluding ILUC). These margins are for an average Midwest producer using RBD soybean oil, based on spot prices.

Key impacts on production and feedstock prices:

- Tax credits do not have a direct impact on the price of soybean oil or corn as these prices are set by global supply and demand dynamics in the vegetable oil or grains complex as the U.S. is a surplus producer.

- Changes to the tax credit or mandate can lead to short term price changes if demand from domestic biodiesel producers increases. However, once the new level of demand has been reached, prices will settle again to an equilibrium.

- Demand for BBD in the U.S. is set primarily by the RFS so tax credits do not have a major impact on demand although they can cause short term market shifts or improve competitiveness of biodiesel against petroleum-based diesel.

- Under 45Z, the credit incentivizes [sic] domestic production and domestic feedstock use which will see an increase in the use of U.S. soybean oil over imported feedstocks. This increased demand should see soybean oil prices rise, in the short to medium term but it should not have a large impact on the long-term price of soybean oil.

- Under normal conditions neither tax credit flows back directly to the feedstock.

BTC Summary

The BTC saw the $1/gallon value spread through the supply chain. Under “normal” conditions producers and consumers/blenders saw as much or more of the benefit than producers.

Under abnormal conditions of either tight- or over-supply, the credit value moves either up or down the supply chain. However, the market cannot exist in these conditions for long periods and must return to an equilibrium state, rebalancing the power in the market.

As an excise credit, the value has been able to flow freely into the supply chain to the benefit of consumers/blenders.

A key difference between the BTC and 45Z credit is that the BTC has historically been claimed by blenders using biofuels (and feedstocks) produced outside of the U.S. This could be circumvented by limiting its use to the blending of local biofuels produced with locally produced feedstocks. This would ensure that benefits remain entirely within the U.S. biofuels supply chain.

45Z Summary

The producer tax credit sees a lower value credit enter the supply chain compared to the BTC. Under “normal” conditions producers are expected to see the most benefit. Thanks to the mechanism of variable credit values and thanks to delayed payments as an income tax credit. The credit gives a competitive advantage to U.S. producers and feedstocks but once the market has reached a new equilibrium under the new, larger market, prices and margins will return to normal levels.

As with under the BTC, under ab-normal conditions of either tight- or over-supply, the credit value will move either up or down the supply chain. However, again, the market cannot exist in these conditions for long periods and must return to an equilibrium state, rebalancing the power in the market.

As an income tax credit, the value is less able to flow freely along the supply chain, benefitting producers at the expense of consumers/blenders.