The first strikes on Iran occurred as this issue was going to print. Oil & Energy summarizes several reports and analyses from that first week.

It is always risky for a monthly publication to provide content on geopolitical upheavals, as the information available is literally “old news” by the time it reaches the readers. However, the first strikes on Iran occurred just as this issue was going to print, and we felt it necessary to acknowledge the anticipated effects it will have on the energy market. More importantly, we wish to express our concern for the men and women of our armed forces, their families, and anyone who may have loved ones in harm’s way.

Shipping and Prices In Dire Straits

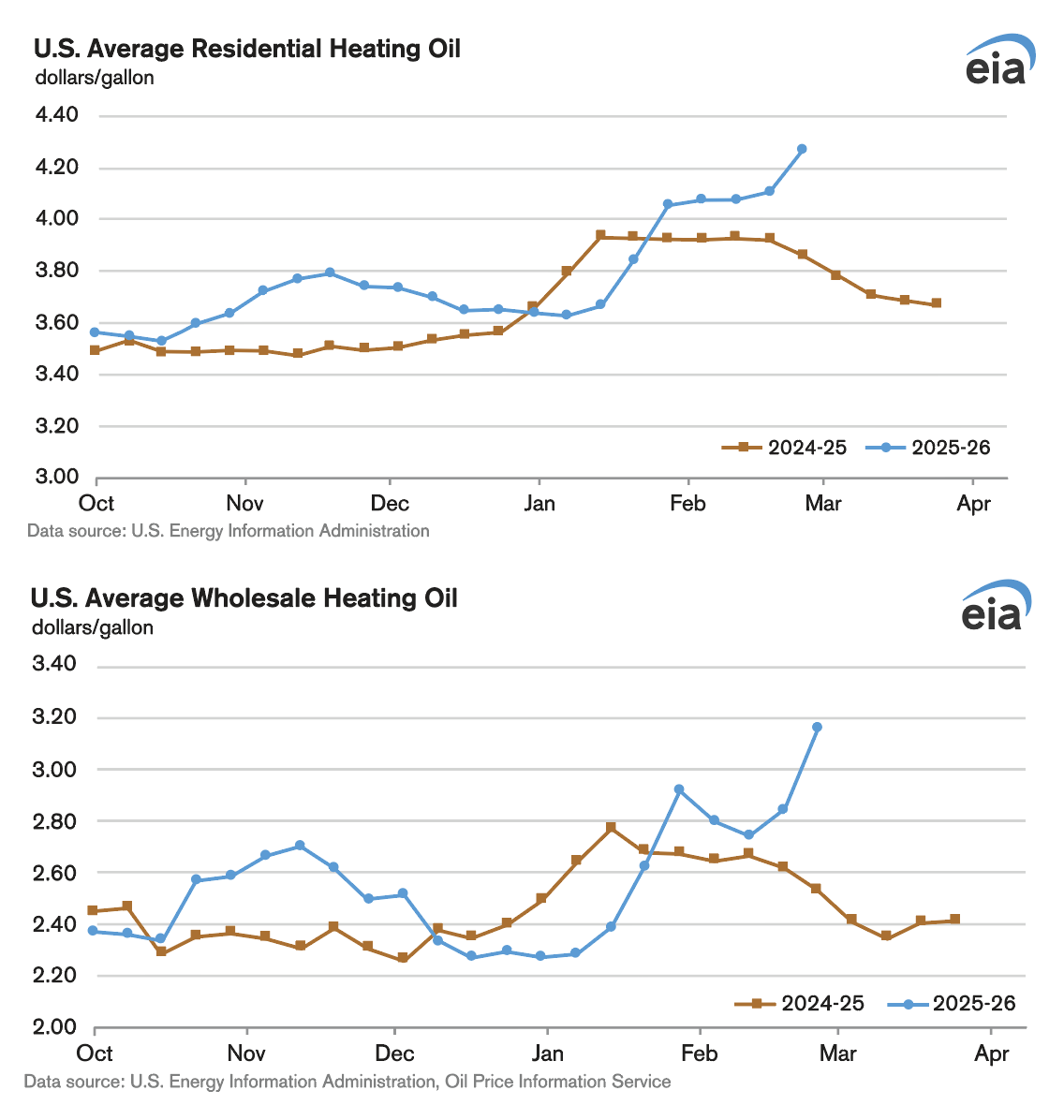

The EIA released its weekly “Heating Oil and Propane Update” on March 4, with pricing data as of March 2, just two days after the first bombs were dropped on Iran.

That short period of time was long enough to see residential heating oil prices increase 16 cents over the previous week, and nearly 41 cents over the previous year. Wholesale heating oil prices jumped 31 cents in the week, and were 62 cents higher than this time in 2025.

While energy prices are always volatile in times of conflict, this war in the Middle East has an added risk: the Strait of Hormuz.

Historically, 20.8 million b/d of oil and products travel the Strait per year, of which 15.4 b/d is crude oil. Most of that oil goes to Asia, and bypass routes have limited capacity.

This 21-mile wide strait was virtually shut down in the early days of the war. Tankers feared crossing the narrow passage, with the New York Times reporting that a senior Iranian official threatened to “set on fire” any ships traveling through. Furthermore, major marine war risk insurance providers immediately began issuing 72-hour cancellation notices for coverage in the Middle East Gulf and the Gulf of Oman, effectively resetting the terms of engagement for any vessel in the region. As negotiators for shippers and insurers attempted to reach some agreement, the estimates were that coverage rates would increase from 25 percent of the vessel’s hull value to 35-50 percent.

With these challenges in place, a formal closure of the Strait of Hormuz was not necessary, as major container lines suspended bookings and directed their vessels to “safe shelter” areas.

In response, President Trump posted to his Truth Social that he had “ordered the United States Development Finance Corporation (DFC) to provide, at a very reasonable price, political risk insurance and guarantees for the Financial Security of ALL Maritime Trade, especially Energy, traveling through the Gulf. This will be available to all Shipping Lines. If necessary, the United States Navy will begin escorting tankers through the Strait of Hormuz, as soon as possible.” At the time of publication, additional details on this insurance, its costs, or naval escorts were not available.

Analysis: What Could Come

The S&P Global Energy Crude Oil Markets Team, led by Vice President Jim Burkhard, released an analysis of the potential risks of the conflict on March 2, noting that it “has the potential to be the largest oil supply disruption in history if oil flows via the narrow Strait of Hormuz remain low or come to a halt.”

S&P Global Energy Commodities at Sea data reported that on March 1, only 5 oil tankers transited the Strait, compared to the average of 60 per day. A supply disruption of this magnitude, or even at a lesser level, could affect between 7 million b/d of crude and products to as much as 15 million b/d, they added.

“While not certain, the risk is real. The potential impact on global oil supply and the world economy could be so significant that it is difficult to imagine a worst-case scenario—no tankers transiting the Strait of Hormuz—lasting more than a short while, but it could.” Burkhard said.

The S&P report concluded: “Before the outbreak of hostilities, the S&P Global Energy outlook expected global crude oil production to exceed demand by 1.4 million b/d in the first quarter of 2026 and by an average of 1 million b/d for the year overall.

“However, the reduction in tanker traffic and the targeting of energy infrastructure have the potential for a shift—and possibly a historic one—from a surplus to a large deficit, which would mean prices high enough to ration scarce supplies and lower demand.”